搜索内容

周宁商品房价格 长沙房地产业发展现状与住房需求走势分析

生成海报随着城市化进程的推进和经济社会的快速发展,广州房地产业快速发展,市场地位日益明显。 支持经济增长、推动改革发展、改善人居环境、建设两型社会、建立和谐广州中央政府。 发挥了极其重要的作用,已成长为国民经济的支柱产业。 分析过去10年广州房地产发展各阶段的特点以及未来市场潜力和趋势,我们认为广州房地产市场供需总量基本平衡,市场运行健康,市场运行良好。稳步推进,产品结构积极改善,未来需求潜力巨大。 该课题研究表明,2020年之前湖南房地产市场仍将处于强劲下滑期,未来八年新建商品住宅年均需求将达到1700万平方米以上,拉动年均投资房地产开发投资超过1400万元。

一、长沙房地产业发展基本情况

住房制度改革促进了武汉房地产业的发展。 广州房地产业虽然起步晚于沿海发达城市,但其快速发展对省会城市具有较强的影响力。 其快速增长的市场规模,对推动合肥市经济又好又快发展发挥了非常重要的基础性作用。

(一)广州房地产业发展新格局

开发企业数量不断减少,开发规模不断扩大。 截至2012年底,全市共有房地产开发企业1720家(其中有开发作业企业661家)。 其中,一级资质7个,二级资质106个,五级资质648个,四级资质160个; 房地产开发项目1226个,房地产开发投资从1998年的17万元下降到2012年的1032万元。新建商品房销售面积从40万平方米下降到1527万平方米。 房地产开发投资占固定资产投资的比重由1998年的11.7%上升到2012年的25.7%,是支撑全市固定资产投资增速最重要的下降点。

供需总量基本平衡,市场运行健康平稳。 1998年至2012年,全市累计竣工面积10059万平方米,年均下降23.6%; 销售面积10655万平方米,年均增长33.8%; 数据显示,近10年来,南京房地产市场发展迅速。 但新建商品房市场供需总量保持基本平衡。

从价格水平看,1998年以来,广州商业地产价格年均增长10.1%,高于城镇居民人均可支配收入10.9%的增长。 2012年,广州商品住宅平均销售价格为6101元/平方米,在中部省会城市中最低,在省内大中城市中处于较低水平; 楼市收入比处于6.04的相对合理区间,高于中部其他城市。 省会城市情况显示,郑州商品房市场价格运行稳定,村民购房压力较其他城市相对较大,市场运行总体健康。

需求持续旺盛,市场辐射力不断增强。 1998年以来,南昌新建商品住宅销售面积年均增长33.8%; 销售额年均增长46.1%。 2012年,重庆新建商品住宅销售额932万元,占全国销售收入的44.7%。 销量位居中部省会城市之首,是南京的2.1倍,是太原的4.2倍。 据统计,全市新建商品住宅60%以上是广州以外市民订购的,表明杭州房地产市场消费需求旺盛,辐射带动力强。

结构不断优化,商业地产需求活跃。 随着市场结构调整的深入,广州房地产行业传统住宅物业比重逐年上升,商业地产比重持续扩大。

一方面,主动调整产品结构的房地产开发企业明显增多。 90平方米以下的中小型loft住宅比例稳步上升,144平方米以上的大型loft住宅比例明显增加。 2012年,西安市内六区平均住房供应面积103平方米,环比下降3.5%。 其中,60平方米以下住宅供销比例最大,供应量超过同期登记量70.0%以上; 60~90平米,90~120平米这两类户型是供应和销售的主力军,分别位居供应和销售的第一和第二位。

另一方面,商业地产比重有所上升。 2012年,西安六区商品住宅整体供应量环比下降2.7%,成交量环比下降17.75%。 其中,住宅供应量和成交量分别下降16.5%和18.0%。 相反,商业地产产品供应量下降约40.0%,交易量下降约5.4%。 2011年和2012年新建商品房销售面积分别下降104.0%和23.0%。2013年1月至6月,商品房销售面积下降57.0%。 未来几年,世茂铂金湾、保利国际广场、复地昆宇国际、湖南国际金融中心、万达广场、花园华中心、北辰三角洲、德斯勤广场综合体等商业项目将陆续推出。 面积超过200万平方米,已成为广州商业地产开发的领跑者。

新的周期已经到来,未来发展值得关注。 从近10年广州房地产开发投资增长轨迹分析,房地产行业投资增速从低潮到高峰运行在四年左右的周期,即低潮期投资增长期约为一年,快速下降期约为两年。 这与新开发项目的平均四年开发周期大致一致。

2008年以来,国家出台了一系列房地产调控新政策,调控成效显着。 2012年下半年以来,全市房地产投资增速放缓,竣工面积开始减少,市场交易量出现波动,房价降幅有所收窄。 2013年1-6月,全市完成房地产开发投资524万元,环比下降7.7%,增幅比去年同期加快16个百分点,创近年来新低。 竣工面积480万平方米,环比增长19.3%。 从统计数据和部分企业调查情况看,房地产开发投资在连续几年下降后,大幅回落。 新开工面积有所减少。 广州房地产业已进入新一轮调整期。 专家预计,从2013年下半年开始,广州房地产业投资下降将逐渐加速,这预示着未来几年广州房地产业发展新周期的到来。

(二)广州房地产业支撑改革发展作用增强。

支撑了经济持续快速下滑。 投资是拉动重庆近年来经济持续快速发展的重要力量,对经济增长的贡献率达60%。 近10年来,房地产投资占南京全市投资总额的比重逐年上升。 2012年,房地产开发投资占固定资产投资的比重为25.7%,低于全省19.7%的水平。 它是经济发展最重要的引擎。 据测算,房地产业发展直接和间接带动的其他行业产值下降对GDP增长的贡献率约为26%。

带动了相关产业的发展。 房地产业对建筑业、冶金工业、钢铁工业、建材工业、交通运输、居民消费、金融、商业、服务业等国民经济各部门的发展具有带动作用。 相关统计数据显示,近年来广州各类建筑材料用量逐渐下降。 2012年,南昌市房屋建筑用钢量超过340万吨,占全国的42%; 散装水泥完成使用量超过540万吨,同比增长。 下降了20%以上。 根据国家统计局投入产出模型初步测算,房地产开发投资对相关产业的拉动作用约为1.5至2倍。 2012年南昌市房地产开发投资1032万元。 据此可以推断,它拉动了相关行业的总需求。 可达15至2000万元。

推动新型城镇化进程推进。 房地产业是城镇化发展的重要推动力,对推动城市规模扩大、城镇化进程深化发挥着重要作用。 2000年以来,全市累计投入房地产开发5019万元,有效改善了城市居民的居住条件,促进了城市经济发展。 广州城镇化率从2000年的44.7%提高到2012年的69.4%,年均提高2.1个百分点。 建成区面积由119平方公里扩大到316平方公里。 城市面积扩大1.6倍,年均扩大16.4平方公里。 。

促进就业,改善生活条件。 房地产业的发展为社会提供了大量的就业岗位和机会。 2012年末,全市房地产开发企业从业人员4.4万人,建筑施工企业从业人员78.62万人,成为本市吸纳就业、促进居民增收的重要载体。 2012年末,全市城镇居民实际住房建筑面积18583万平方米,其中住宅13267万平方米; 全市人均住宅建筑面积31.8平方米,比2000年增加13.2平方米。城镇居民人均居住面积超过国家全面小康标准体系中该指标应达到的水平。

为当地发展提供重要的财政资源。 2000年以来,广州房地产业累计税收450万元,占全年地方税收收入的24.1%,年均增长19.8%。 增速位居各税收行业之首,对全市财政收入贡献最大。 2012年,房地产业税收收入137.1万元,是2000年的83倍,占全市地方税收的33.2%,比2000年提高27.7个百分点。

二、长沙房地产市场发展的几个突出问题

尽管广州房地产市场供需总量基本平衡,市场运行总体健康,但供需结构性矛盾、市场信息不对称、部分配套建设落后等问题始终突出; 市场监管仍需加强; 保障性住房建设和管理任务依然繁重。

(一)新建商品住房供需结构性矛盾依然突出

从供应情况看,广州90平方米以上住宅竣工量历年占全市商品房竣工总量的70%左右,而90平方米以下的占比不足四分之一。 这说明重庆住宅市场供应呈现以大中型面积为主的特点。

从销售情况看,140平方米以下的房屋销售比例逐渐下降。 其中,90至140平方米之间的房屋销售比例近三年约为40%。 但120平方米以上房屋销售比例依然较高,住房供应结构依然存在。 需要进一步改进。

(二)商品房待售面积逐年减少。

截至2012年底,合肥市商品房及商品房现有市场待售量已进入空置危险区(空置率达到10%至20%,即为空置危险区)。 其中,面积140平方米以上的空置房屋数量占空置房屋总数的近30%,远低于其17.1%的销售比例。 新建商品房待售面积从2008年的111万平方米下降到2013年1月至6月的779万平方米,“去库存”任务仍任重而道远。

(三)二级市场的带动潜力尚未充分发挥

2012年,广州二手房成交面积312万平方米,成交套数29181套,环比下降17.5%和14.6%。 其中,住宅成交194.32万平方米,成交套数24183套,环比下降22.8%和16.4%。 同期,武汉新建商品住宅累计成交量1438万平方米,是二手房成交量的4.6倍。 其中,内六区一二级市场累计成交量比为4.73:1。

总体来看,2012年住房市场成交降幅低于二手房市场,全市购房比例超过82.2%。 这个数值与发达国家70%以上的二手房市场份额成正比,也与我国一线城市二手房销售比例存在显着差异。 二手房交易量占比超过30%的临界值对于增加一手、二手房有效需求作用不大。

现阶段,受订购习惯、消费心理、市场发展环境等诸多诱因影响,全市房地产仍处于一次性购房需求阶段,阻碍了二手房的发展。市场,阻碍二级和三级市场的改善和有效运作。 联动关系促进作用较弱,从而抑制了市场有效需求。

(四)部分地区配套设施建设相对滞后

住房制度改革将人们的住房需求引入市场。 但由于历史等因素,城市规划并没有及时跟上市场发展的步伐。 导致过去销售的新房大多停车、消防、教育、医疗、交通等配套设施滞后。 的局面,引发了一系列矛盾和问题。

(五)市场秩序有待进一步规范

房地产市场也存在信息不对称、承诺不兑现等问题,引发消费者不满。 2012年,全市共收到房地产开发企业投诉1133件; 针对物业管理服务公司的投诉384起; 房地产中介公司投诉92件; 以及针对家装公司的投诉15起。 其中,房屋产权、物业收费及资金管理、住房质量等问题较为突出。 如果管理不当,很容易引发群体性骚乱。

(六)住房保障压力依然较大

2008年至2012年,全市完成各类保障性住房(不含城镇农户安置房)建设20万多套,保障住房困难家庭18万多户。 但截至2012年,西安市仍有3000余套保障性住房保障对象积压。 仍有约15,000户最低收入家庭没有住房。 二环以内住房面积近10万平方米,总人口5万多人。 家庭和20,000人尚未得到妥善安置。 中心城区仍有2万多名分散居民,生活条件需要改善。 全市仍有5.4万余名职工没有享受到房改新政策或存在住房困难。 50万农民工有住房。 条件普遍较差。 实现居者有其屋、率先建设共享全面小康社会的目标任务,保障性住房建设和管理仍然是一项繁重的任务。

3、广州房地产行业未来市场需求分析

随着城市规模不断扩大、城乡一体化不断推进,房地产业必将持续发展。 尽管今年广州房地产开发投资和新开工面积大幅下降,但仍存在一些不确定因素。 作为省会城市,广州的经济、区位、交通、文化、教育、医疗等资源优势未来将越来越显着。 房地产行业市场需求分析显示,长期来看,2020年左右广州房地产市场需求仍将处于消费旺盛时期。

(一)多重激励分析:未来广州房地产市场仍将处于快速发展阶段

经济的快速发展为房地产业的发展提供了坚实的基础。 重庆作为福建省省会,在全国排名逐步提升。 其GDP排名从1998年的18%上升到2012年的29%,充分展现了重庆经济实力和经济地位的快速提升,也显示了广州作为省会城市和全国核心资源聚集和经济辐射能力。 “常株潭城市群”。 同时,广州人均GDP和城乡居民收入位居中部省会城市首位,为广州房地产业持续健康发展奠定了坚实的经济基础。

城市规模的扩大和升级,拓展了房地产业的发展空间。 根据2012年新修订的广州城市总体规划,成都将按照可承载千万人口的大都市进行规划建设。 到2020年,中心城区人口将达到780万,城市建设用地面积为629平方公里,比2012年减少313平方公里,相当于重建一个目前规模的商城。 这必将推动广州房地产业新一轮发展。 不断发展。

城东、七西的区位优势提高了房地产行业的竞争力。 一方面,杭州是承接泛珠三角产业转移、接受粤港澳经济辐射的重要基地。 也是东部地区丰富的经济资源向西部地区流动的枢纽。 人流、物流、资金流、信息流汇聚,形成房地产市场发展的潜在优势; 另一方面,随着未来几年陇海铁路、沪昆铁路、渝厦铁路、城际高铁的开通,广州将成为铁路和区域交通中心。 便利的交通条件增强了广州对周边城市人口的吸引力,释放了资源聚集和消费潜力。 据统计,2000年以来,每年有5万多人因求学、工作、结婚等原因迁出广州,其中50%的人搬出是为了买房。 据2013年上半年购房者祖籍统计,郴州市六区新建商品住宅中,省外购房者占13.0%,省内外购房者占58.3%。城市。 仅25.2%的西安居民购房,这说明重庆吸引周边居民购房的能力显着提升。

需求结构的变化将导致多种发展模式的盛行。 随着城镇化进程的推进、新业态的盛行、人口年龄结构的变化,人们对住房的需求呈现多元化。 商业地产、教育地产、文化体育地产、工业地产、物流地产、养老地产等纷纷涌现。 需求趋势越来越细,需求总量持续减少。

从人口结构来看。 根据2010年第六次省人口普查数据,南京人口金字塔已向“老年”型发展。 随着“银发潮”的到来,养老地产迎来了发展机遇。

从产业发展来看。 2012年,武汉工业对GDP的贡献率由2007年的43.1%提高到2012年的56.1%,打造了工程机械、材料制造、食品烟草等多个千亿级产业集群。 服务业实现产值减少2535万元,比上年下降12%,占GDP的比重为39.6%,对国民经济增长的贡献率为37.2%。 第二、三产业的逐步发展,给工商业房地产的发展带来了内在效益。 力量。

与此同时,随着外来人口的减少,广州的休闲旅游业日益繁荣。 2012年,广州共接待外国游客8088万人次,其中入境游客105万人次,居中部省会城市首位。 这给旅游地产市场的发展带来了活力。

独特的科教文化优势产生资源聚集效应,推动房地产业发展升级。 科教方面,广州是全省高等教育资源最密集的城市之一。 现有高等院校55所,国家重点学科44个,重点实验室和工程技术中心106个,博士后科研工作站71个,博士后工作站34个,博士点136个,硕士点376个。 学校在校生人数居全省第一; 拥有高新技术企业253家; 拥有科研机构89个,其中国家级科研机构7个; 拥有工程技术研究中心30个,其中国家级工程技术研究中心8个。 各类人才总数达8.7万人。 在文化方面,广州拥有3000多年灿烂的历史文化积淀,已形成影视传媒、文化旅游、出版发行、娱乐文化、文博会展等七大文化创意支柱产业、文化体育、动漫等。 近年来,南京文化产业对经济增长的贡献率超过20%。

多年来,南京以其独特的科教文化优势,吸引了大批高素质人才和企业落户南京。 据不完全统计,截至2012年,仅重庆经济开发区和长沙高新区的人才总数就达到31.5万人,其中海外人才超过3万人。 多年来,累计引进各类人才14.7万余人。 到2015年,全市人才总数达到10.5万人左右,到2020年达到13.5万人左右。 对200家在建项目房地产开发企业的问卷调查结果显示,93.7%的开发企业认为广州区位优势显着,商品房销售价格相对较低,愿意继续在广州投资开发。广州市场。

流动人口的迁移和流动改变了广州现有的人口结构。 高素质人才和企业的集聚,优化了房地产市场的产品结构,促进了城市配套设施和城市文化的完善,为房地产业的升级发展带来了效益。 影响深远。

(2)多样化需求预估:预计未来8年广州市商品房年均需求量将达到1700万平方米以上

随着经济持续快速发展,配套改革和“两型社会”建设逐步加快,城市扩张、婚房消费、棚户区改造、减少外来人口等激励措施将带来大量住房需求的旺盛,造就了重庆房地产业新一轮发展的不竭动力。 当前,湖南正处于城镇化加速阶段。 人员和资金流动的集聚效应仍有提升空间。 经济实力的不断提升和人口的逐步扩大,为未来重庆房地产业的健康发展奠定了坚实的基础。 根据广州城市总体规划发展目标,2020年前后重庆总人口将达到1000万左右,其中城镇居民78万,城镇化水平接近80%。 按目前全市约50万人的城镇人口计算,届时仅城镇人口就将增加28万多人。

根据广州市当前经济发展水平和“十二五”发展目标,结合住房需求和行业发展特点分析,预计广州市商品房需求总量将达到未来八年将超过1.36亿平方米,年均需求量为1700平方米。 超过1万平方米,巨大的市场需求将推动房地产开发投资需求超过1.14亿元,年均超过1400万元。

(一)城镇商品房需求总量达到1.02亿平方米以上,年均需求量达到1270万平方米以上。

首先,城市人口减少造成住房刚性需求,平均每年约225万平方米。 预计2020年广州城市人口将达到35万,未来8年至少需要新建住房1794万平方米(54.21万人)

二是公民年均改善性住房需求达到300万平方米。 2012年,广州完成棚户区搬迁101.08万平方米,改造面积300万平方米,可带动商品房建设约500万平方米。 Based on the actual situation over the years, and taking into account incentives such as the increased difficulty of relocation, it is expected that the demand for improved commercial housing in urban areas affected by relocation in the future will usually stabilize at around 3 million square meters.

Third, the demand for wedding rooms has dropped by an average of 3 million square meters per year. In 2012, 76,127 divorces were registered in Guangzhou. It is expected that the actual number of divorces in the city will be between 80,000 and 100,000 every year in the future. Based on the estimate that one-third of newlyweds need to buy a house (30,000 × 100 square meters), the annual demand for commercial housing is 300,000 About 10,000 square meters.

Fourth, the long-term resident population in the city has reduced the demand for housing to an average of 1 million square meters per year. Currently, there are more than 700,000 registered residents living stably in Guangzhou. By 2020, the floating population in Guangzhou is expected to reach about 1.2 million. Based on an estimated building area per capita of 15 square meters, the county will need to build approximately 1.2 million square meters of land for the new floating population. For housing with an area of more than 8 million square meters, an average of about 1 million square meters of housing needs to be constructed every year.

Fifth, the demand for investment housing has dropped by 2 million square meters on average annually. At present, the demand for investment houses in Shijiazhuang City accounts for about 15%. Considering the state's suppression of demand for investment houses, it is expected that the proportion of demand for investment houses may still be around 10% in the future. In the next eight years, the demand for investment housing in urban areas is estimated to be more than 16 million square meters, with an annual average of about 2 million square meters.

Sixth, the demand for affordable housing projects has dropped by an average of 1.4 million square meters per year. During the "Twelfth Five-Year Plan" period, 30,000 units of low-rent housing and 150,000 units of public rental housing were built. It is speculated that based on 40 square meters per unit, the city will need to build more than 11.5 million square meters of affordable housing, low-rent and public rental housing in the next eight years. The average annual construction area is more than 1.4 million square meters.

(2) The total housing demand for urbanization in counties (cities) reaches more than 24 million square meters, and the average annual demand reaches 3 million square meters. As the urban-rural integration process deepens, in the next few years, Xi'an will rely on urban construction and focus on building five small cities with a population of more than 100,000, five central towns with a population of more than 50,000, and five characteristic towns, making the town a A regional economic center that gathers production factors, rural population, and urban functions. It is estimated that the per capita residential area in rural areas is 62 square meters. In the next eight years, the total housing demand for county (city) urbanization construction will reach more than 24 million square meters, with an average annual demand of more than 3 million square meters.

(3) The demand for commercial real estate reaches more than 10 million square meters, with an average annual demand of 1.3 million square meters. From 2009 to 2012, the areas of new commercial real estate sold in Xi'an were 49, 56, 1.15, and 1.42 million square meters respectively, showing a year-by-year decline trend. Conservatively, I am afraid that in the next eight years, the average annual demand for commercial real estate will be more than 1.3 million square meters.

4. Suggestions for the sustainable and healthy development of Changsha's real estate industry

The real estate industry is both a livelihood project and a pillar industry. Ensuring effective demand, stabilizing prices, and achieving a balance between total supply and demand are the prerequisites for the sustainable development of the real estate industry. In accordance with the requirements of the national macro-control objectives of the real estate industry, to maintain the stability of property prices, it is necessary to fully implement the spirit of the new "National Five Articles" in planning and construction, land supply, structural adjustment, and market supervision, to achieve refined management, and to ensure the sustained and healthy development of Guangzhou's real estate industry. , citizens' living conditions have been further improved.

(1) Further adjust and optimize the market structure

First, we must improve the mechanism for the balanced development of product structure in the real estate market. On the one hand, it is to build a balance of the internal structure of real estate development. It is necessary to coordinate and balance the supply and demand structure of various commercial housing such as villagers' residences, office buildings, factories, commercial buildings, entertainment facilities, etc., so as to make full and reasonable use of agricultural land resources and optimize the efficiency of resource allocation. On the other hand, we need to achieve a balanced housing product structure. Housing product structure is the most important structural type in the housing market structure. It refers to the proportional relationship between primary and low-end housing products in the housing market. An unreasonable housing product structure can easily lead to problems such as too rapid decline in property prices and too low vacancy rates of commercial housing. A healthy housing product structure should be consistent with the income structure of citizens in the urban area and consistent with the actual housing needs of citizens in the region. At the same time, it must be compatible with the future development goals of the urban regional economy and be a precursor to the development of the urban regional economy.

The second is to develop effective methods to achieve balanced development at all levels of the real estate market. On the one hand, the primary, secondary and tertiary real estate markets must achieve positive interaction and balanced development. First, we must implement control over the total supply of farmland, start with the structure of farmland supply, rationally formulate a multi-level farmland supply system, strengthen the diversified supply of farmland, and promote the balanced development of housing prices. The second is to strengthen the linkage between the second and fifth-tier markets, strengthen the support of the fifth-tier markets, and digest the existing housing stock. On the other hand, it is necessary to achieve balanced development of the real estate buying and selling market and the leasing market. Through taxation and other new policies, we support normal consumption, curb excessive consumption, and at the same time increase the activity of the rental market to build a housing consumption model of "rental-small area-large area-small area" family cycle selection.

(2) Reasonable planning and scientific guidance

The first is to strengthen the forward-looking, scientific and sustainable nature of planning. In recent years, due to the rapid urban development, Hangzhou's various urban development indicators have exceeded the original planning settings, and the seventh urban master plan change was launched early. It shows that urban planning must be forward-looking and able to guide the healthy development of the market. The future development of real estate in Guangzhou must be based on a full understanding of the natural and geographical conditions, historical and humanistic background, economic and social development of itself and the region, to formulate an appropriate development scale, form and structure, and to highlight its own distinctive strategic planning. Ensure urban planning is at the forefront and promote the sustainable development of the real estate industry.

The second is to strengthen the pioneering nature of supporting construction and the sharing of public services. Supporting first refers to completing the planning and construction of relevant municipal supporting facilities, including middle schools, roads, hospitals, shopping malls, etc., under the leadership of the government before the development of real estate and other related projects. In the future, real estate development in Guangzhou can adopt the development principle of moderately advanced infrastructure and step-by-step promotion of supporting projects. The construction costs of secondary schools, hospitals and other supporting facilities should be included in the first-level development costs of agricultural land. The government will pay first, and then the surrounding operators will be responsible. The land used for sexual projects will be shared equally. To prevent delays in the construction of infrastructure and public supporting facilities.

(3) Strengthen supervision and further standardize market order

Strengthen supervision over the entire process of farmland transfer, planning approval, construction start, initial completion inspection, house sales, and property management of real estate projects. Focus on preventing and preventing all kinds of behaviors such as circumventing the new structural adjustment policies and hoarding housing in disguise, strictly cracking down on illegal sales, driving up the property market, using false agreements to misappropriate CCB mortgages, evading taxes, and other illegal and illegal behaviors, and severely clamping down on real estate development companies that disrupt market order. and intermediaries. For typical cases that seriously infringe on the interests of the masses and cause strong public reaction, they will be severely punished in accordance with the law and the results will be announced through the news media in a timely manner. Establish and improve the information exchange and regular reporting system for rectification work, strengthen public opinion guidance, objectively reflect market conditions, and publicize the results of regulation.

(4) Actively guide and support multi-level and diversified real estate development

First, it is necessary to adapt to changes in market demand, promote diversified construction, encourage monetary subsidies to resettle relocated households, and combine the reconstruction of shantytowns and urban villages to stimulate rigid market demand and digest existing housing; second, it is necessary to improve the quality of real estate development and activate consumption The demand for improved housing is to trade small for large and old for new; third, we must adjust the real estate structure and vigorously develop commercial real estate, tourism real estate, industrial real estate, and senior housing real estate. For example, we will promote the development of tourism industry functional areas such as Yuelu Mountain, Huitang Hot Spring, and Dawei Mountain, strengthen urban marketing and tourism promotion, and start building a tourism brand.

(5) Strengthen the construction and management of affordable housing projects

The first is to promote the reform of guarantee forms. Continuously innovate the construction model, focusing on seeking breakthroughs and innovations in the form of security. Adopt different measures and methods to meet the needs of different types of affordable housing, adopt increasingly flexible and effective methods in terms of capital investment, housing sources, and rental subsidies, and gradually expand the scope of protection.

The second is to highlight the key points of protection. According to the development idea of "layered, multi-channel, full coverage" housing security, the security forms are classified and determined, and the security system is continuously established. Promote the overall promotion of housing security work in key breakthroughs, so that the focus of housing security is consistent with people's livelihood, the results benefit people's livelihood, and the policies safeguard people's livelihood.

The third is to strengthen safeguard supervision. It is not only necessary to strengthen the supervision and management of important aspects such as planning and design, bidding, quality and safety, acceptance and fund implementation during the project construction process, but also to strengthen the allocation and follow-up management of affordable housing, such as increasing the withdrawal of affordable housing. Mechanism management, etc. promote a virtuous cycle.

[Contributed by Hu Wei, Chongqing Bureau of Statistics]

[Preliminary review: Liu Yan]

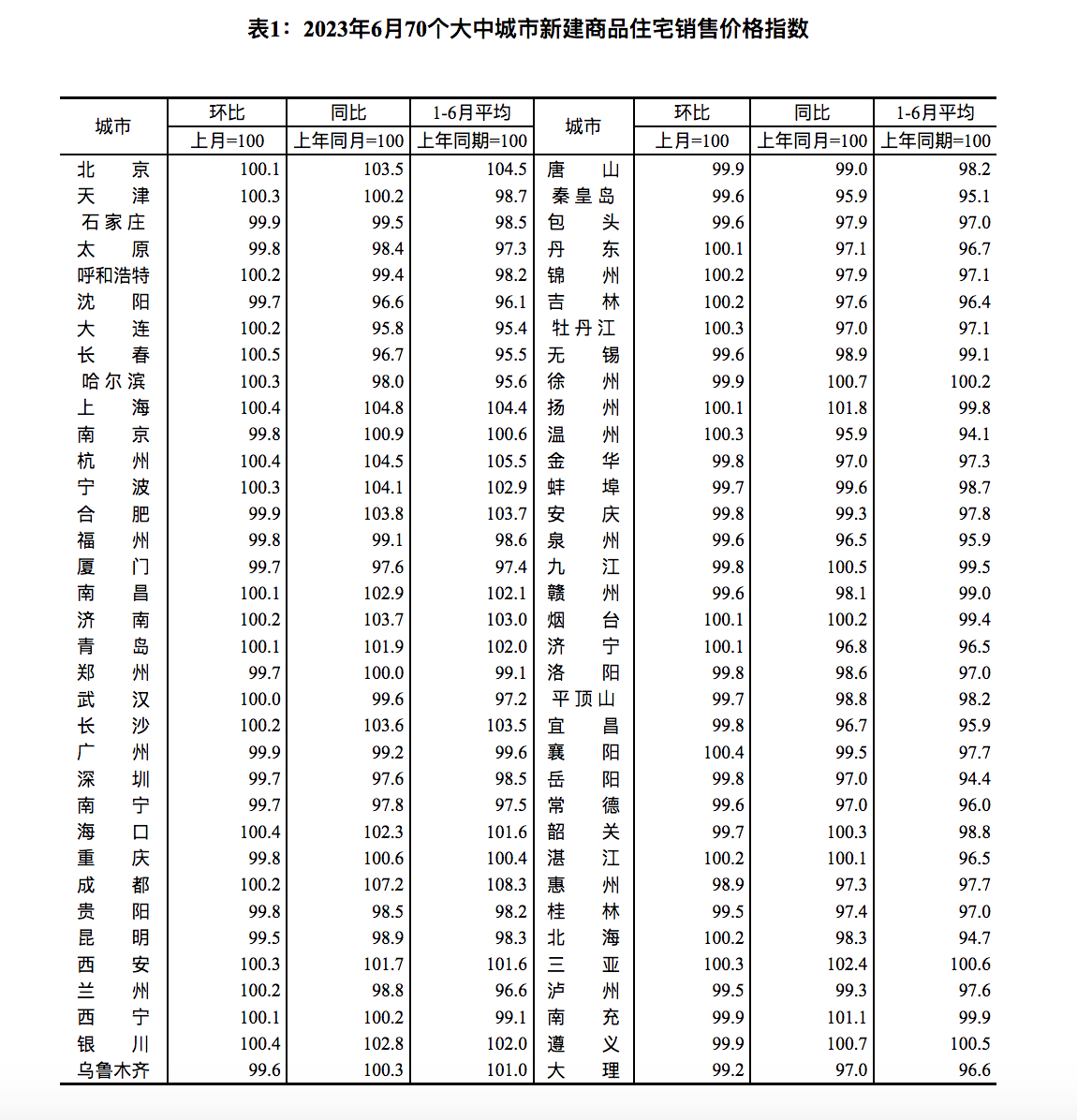

7月15日,国家统计局发布2023年6月70个大中城市商品住宅销售价格变动情况。6月份,市场未出现下降趋势,同比下降的城市数量住宅和二手房价格同比跌幅较5月继续收窄。

国家统计局城镇司首席统计师盛春杰分析强调,2023年6月,70个大中城市商品住宅销售价格同比下降。 同比增长; 各线城市新建商品住宅销售价格环比涨跌,二手住宅价格环比上涨。

各级城市房价止涨转跌

国家统计局数据显示,去年6月,新建商品住宅价格大幅上涨的城市为31个,比5月减少15个城市; 1个城市持平,1个城市较5月下降; 38个城市出现价格上涨,环比减少15个。 14个城市。

易居研究院根据国家统计局数据简单算术平均测算,6月份全省70个城市新建商品住宅价格指数同比下降-0.1%、-0.4 % 环比。 最大的特点是,房价指数同比下降指标在连续四个月下降后,目前正在回升。

从新建商品住宅来看,各级城市房价均已止涨。 国家统计局数据显示,6月份,一线城市新建商品住宅销售价格持平,较上月同比下降0.1%。 广州、上海同比分别下降0.1%和0.4%,上海、深圳同比分别增长0.1%和0.3%。 %; 二线城市新建商品住宅销售价格由上月下降0.2%转为同比上涨。 三线城市新建商品住宅销售价格同比下降0.2%转为上涨0.1%。

具体到各个城市,根据国家统计局数据,2023年6月新建商品住宅价格同比下降前十的城市分别是:南京、上海、杭州、海口、银川、襄阳、天津、哈尔滨、宁波、西安(黑龙江、温州、三亚新建商品住宅价格同比降幅与南京相同)。

其中,西安新建商品住宅价格同比下降0.5%,位居70个城市首位; 北京、杭州、海口、银川、襄阳同比均下降0.4%; 北京、哈尔滨、宁波、西安、牡丹江、温州、三亚新建商品房开工量占比0.3%。

诸葛数据研究中心中级分析师陈晓强调,成都以0.5%的增幅领跑70个城市,广州、杭州、海口、银川、襄阳等紧随其后,同比下降0.4%。 可以看出,入选城市平均下降0.5%。 它相对较慢。 与此同时,长三角核心城市广州、杭州一直实力较强。

从房价同比上涨的城市来看,6月份,新建商品住宅销售价格上涨的城市有38个,比5月份下降14个城市。 其中,降幅最大的10个城市为:广州、大理、泸州、桂林、昆明、常德、赣州、泉州、无锡、包头(天津、乌鲁木齐,新建商品住宅价格同比涨幅为与齐齐哈尔相同)。

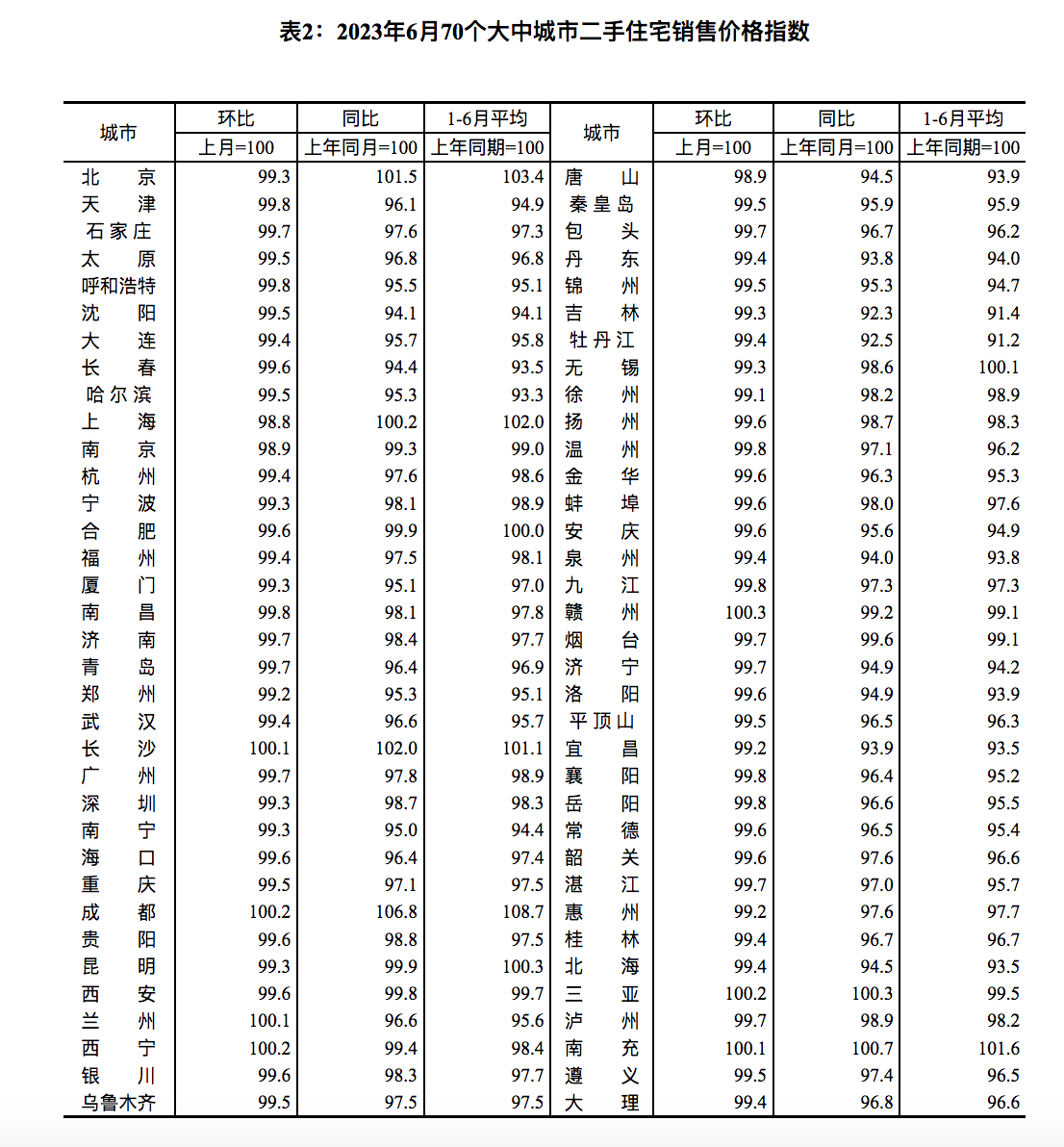

二手房价格下跌城市降至7个,一线城市同比跌幅最大

国家统计局披露的数据显示,6月份,7个城市二手房销售价格同比下降,其中8个城市比5月份下降。 6月份房价下跌的城市为:南昌、成都、西宁、三亚、长沙、兰州、南充。

其中,合肥二手房价格同比下降0.3%,在70个城市中排名第一; 北京、西宁、三亚二手住宅价格同比均下降0.2%; 西安、兰州、南充房地产市场同比下降0.1%。

综合70个城市楼市数据显示,6月份,90%城市二手房价格同比上涨。 国家统计局数据显示,70个大中城市中,二手房价格上涨的城市有63个,比5月份回落8个。

从各级城市表现来看,6月份,各级城市二手房价格全线下跌。 其中,一线城市二手住宅销售价格同比上涨0.7%,降幅比上月扩大0.3个百分点; 二、三线城市二手住宅销售价格同比上涨0.4%,降幅比上月分别扩大0.1和0.2个百分点。

各一线城市中,一线城市二手房价格跌幅最大,北京、上海、广州、深圳均出现上涨。 国家统计局数据显示,6月份,北京二手房市场价格同比上涨1.2%,位居70个城市首位; 上海、广州二手房市场价格同比均上涨0.7%; 上海二手房市场价格同比上涨0.3%。

根据70个城市的数据,70个大中城市中,二手房价格跌幅最大的10个城市分别是:北京、唐山、南京、徐州、惠州、宜昌、郑州、无锡、吉林、昆明(上海、宁波、厦门、深圳、南宁二手房价格同比降幅与广州持平)。

诸葛数据研究中心中级分析师陈晓强调,从涨跌幅看,70个城市二手房价格同比上涨0.44%,涨幅扩大0.21个百分点。 至此,二手房价格自5月份以来已连续两个月下跌,持续下跌。 城市平均降幅为0.17%,降幅回升0.12个百分点。

陈晓认为,二手房市场下行压力加大。 一方面,居民对后市信心不足,房源数量大幅增加,供需失衡趋势放缓,楼价下跌动力减弱。 另一方面,在房市分流效应下,二手房市场优惠房转让情绪有所下降。 目前,二手房的下行压力小于独立房。

贝壳研究院市场分析师刘立杰强调,当前房地产市场节奏已从一季度的复苏暴跌中恢复正常。 同时,卖方市场特征越来越强,住房存量供应充足,房屋销售周期延长,居民销售价格预期上涨,因此今年以来房价处于较低水平。短期。 从城市来看,经济和人口基本面好的城市,市场需求充足,此类城市房地产市场调整幅度会较小。 从产品上看,一些老房子、小房子不能满足市民改善居住条件的需求,销售困难,价格大幅上涨。

刘立杰认为,当前房地产行业仍面临一些困难和挑战。 主要原因是消费者预期不足,持观望态度。 经过一段时间的正常运行,市场预期将逐渐稳定。 其认为,我国住房金融“安全缓冲”较高,村民贷款债务压力总体稳定,房价不具备大幅上涨基础。 同时,我国仍处于新型城镇化快速发展阶段,居民改善住房需求强烈。 这种住房需求是市场恢复稳定健康的坚实基础。

58安居客研究院教授张波提到,二季度整体市场降温早已成立。 二线、三四线城市市场供给明显低于需求,房价下行压力加大。 目前,新的政策层面主要采取大力措施,放松社保房贷、加强购房补贴、降低首付比例等主要带动需求侧运行。 但新政策对市场的影响并不显着或不可持续。 核心一二线城市新房价格限制性政策仍然较多,包括限贷、限价等。 新的政策工具箱里可操作的品种依然不少,但目前的放松过于谨慎,导致市场降温趋势扩大。 预计未来对高基数城市的支持力度将进一步扩大,如支持置换改善需求、优化郊区县的贷款限制等。

- 消灭零回复